Markets on Wall Street inched slightly higher ahead of the release of more inflation data from the U.S. government.

Futures for the Dow Jones Industrials and S&P 500 were each less than 0.1% higher before the bell Tuesday.

Home Depot shares rose 1.8% in premarket after the home improvement chain beat profit forecasts but logged its third straight quarter of declining sales. The retailer has been warning about softening sales with mortgage rates still elevated, which makes it more expensive for people to buy a home or remodel their current one.

Meme stocks are jumping again Tuesday, adding to their gains Monday when the man at the center of the pandemic meme stock craze — Keith Gill, better known as “Roaring Kitty” — appeared online for the first time in three years.

GameStop jumped 83% before the bell Tuesday, while AMC Entertainment climbed 75%. BlackBerry rose more than 25% early.

Investors also were watching for indicators on inflation to gauge the direction of economic growth, as well as the strength of the dollar.

Stocks have broadly rallied this month following a rough April on revived hopes that inflation may ease enough to convince the Federal Reserve to cut its main interest rate later this year. A key test for those hopes will arrive Wednesday, when the U.S. government offers the latest monthly update on inflation that households are feeling across the country.

Other reports this week include updates on inflation that wholesalers are seeing and sales at U.S. retailers. They could show whether fears are warranted about a worst-case scenario for the country, where stubbornly high inflation forms a devastating combination with a stagnating economy.

Hopes have climbed that the economy can avoid what’s called “stagflation” and hit the bull’s eye where it cools enough to get inflation under control but stays sturdy enough to avoid a bad recession. Federal Reserve Chair Jerome Powell also gave financial markets comfort when he recently said the Fed remains closer to cutting rates than to raising them, even if inflation has remained hotter than forecast so far this year.

Earnings season has nearly finished, and reports are already in for more than 90% of companies in the S&P 500. But this upcoming week includes Walmart and several other big names. They could offer more detail about how U.S. households are faring.

Worries have been rising about cracks showing in spending by U.S. consumers, which has been one of the bedrocks keeping the economy out of a recession. Lower-income households appear to be under particularly heavy strain amid still-high inflation.

The Biden administration is expected to announce this week that it will raise tariffs on electric vehicles, semiconductors, solar equipment, and medical supplies imported from China, according to people familiar with the plan. Tariffs on electric vehicles, in particular, could quadruple to 100%.

France’s CAC 40 slipped 0.1% in midday trading, while Germany’s DAX shed 0.2%. Britain’s FTSE 100 rose 0.1%.

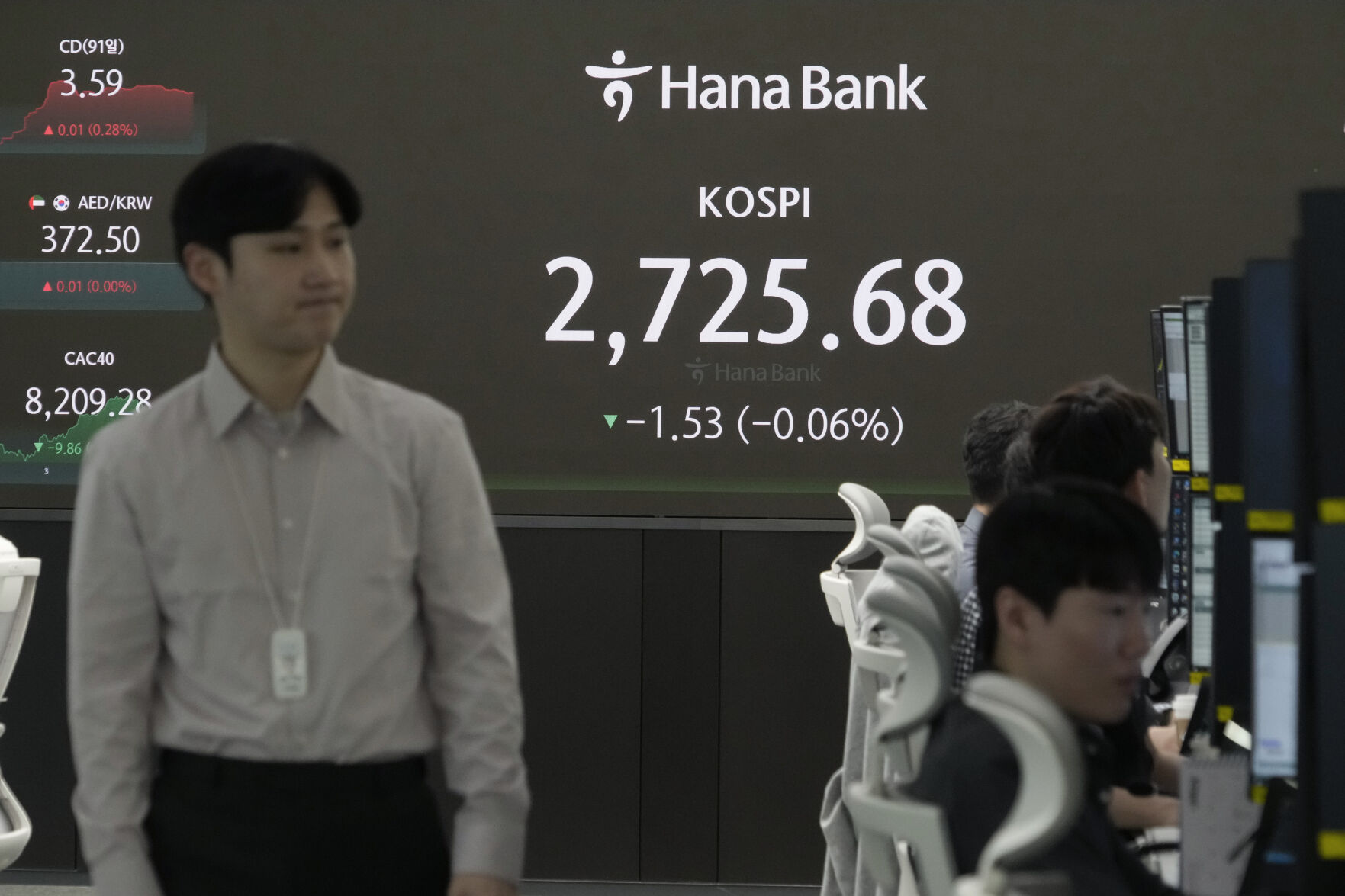

Japan’s benchmark Nikkei 225 gained 0.5% to finish at 38,356.06. Australia’s S&P/ASX 200 slipped 0.3% to 7,726.80. South Korea’s Kospi rose 0.1% to 2,730.34.

Chinese markets were flat ahead of an expected announcement by the Biden administration on raising tariffs on imports from China. Hong Kong’s Hang Seng slipped 0.2% to 19,073.71, while the Shanghai Composite lost less than 0.1%, to 3,145.77.

In other trading, benchmark U.S. crude lost 10 cents to $79.02 a barrel in electronic trading on the New York Mercantile Exchange. Brent crude, the international standard, fell 9 cents to $83.27 a barrel.

The U.S. dollar rose to 156.45 Japanese yen from 156.21 yen. The euro cost $1.0799, up from $1.0790.

On Monday, the S&P 500 edged down less than 0.1%. It remains within 0.6% of its record set at the end of March.

The Dow Jones Industrial Average slipped 0.2% and the Nasdaq composite rose 0.3%.